"It's not so much that people don't like gold anymore - it's that they hate it."

-Dylan Grice

Wednesday, July 31, 2013

Faber and Obesity

The monthly Marc Faber piece came out today. To get right to the question one might ask, he continues to be constructive on gold, both as a long-term investment and as a relative value to any other asset class right now.

But of more interest to me was his discussion of the fact that the American Medical Association is pushing to have obesity categorized as a disease. Faber finds much to object to, but it primarily relates to the idea that people no longer have to take responsibility for their own behavior and the government is provided with yet another avenue to meddle in our lives. By contrast, I thought about it in terms of the David Goldhill book that I read several months ago. One of the big risks with our growing health care system is that everything eventually gets re-defined as a medical condition, and the consequence is that we end up with an ever-expanding list of items that someone else should pay for. To be succinct, the problem with all the government proposals is an underlying assumption that there is a fixed amount of health care that everyone needs. But, as the AMA move should make clear, when someone else is paying, more and more things will get sucked into the vortex of health care, with rising costs to follow.

But of more interest to me was his discussion of the fact that the American Medical Association is pushing to have obesity categorized as a disease. Faber finds much to object to, but it primarily relates to the idea that people no longer have to take responsibility for their own behavior and the government is provided with yet another avenue to meddle in our lives. By contrast, I thought about it in terms of the David Goldhill book that I read several months ago. One of the big risks with our growing health care system is that everything eventually gets re-defined as a medical condition, and the consequence is that we end up with an ever-expanding list of items that someone else should pay for. To be succinct, the problem with all the government proposals is an underlying assumption that there is a fixed amount of health care that everyone needs. But, as the AMA move should make clear, when someone else is paying, more and more things will get sucked into the vortex of health care, with rising costs to follow.

Tuesday, July 30, 2013

Interesting Reads

-First up is the latest installment from Doug Noland at The Prudent Bear. It is full of stats on how much more levered the world has become, and how much higher stock markets have gone, all while we see quarter after quarter of weak GDP numbers. I thought this bit was useful: “A few weeks back the markets were again indicating fragility – and the Fed once again demonstrated its market-pleasing low tolerance for market weakness. The flaw in aggressive QE is the notion that the Fed will be able to back away from market intervention without major consequences. Fed stimulus can spur debt issuance, market risk embracement and speculation. But if that debt is mispriced and predominantly non-productive, the system faces unavoidable debt problems. If speculative leverage is playing a prominent role in inflating securities and asset markets, the system face unavoidable de-leveraging issues. If the already vulnerable household sector continues to load up on mispriced stocks and bonds, there will be negative consequences.”

-Next up is an article from the RT website that details how the U.S. has busted through the debt limit ahead of schedule. So far, it has not gotten much attention. As an aside, one interesting forecast in the Stockman book was premised on the notion that the U.S. no longer has a real appetite for large increases in the outstanding debt load. Thus, the “fiscal cliff” silliness of last year is set to become a recurring soap opera, with politicians always trying to do just enough to keep the ball moving. However, it stands to reason that the impact will be deflationary, with consumers trying to re-trench and saving more in the face of a slowing economy. Thus, we will probably see even more depressing GDP prints over time, even as the Fed tries to print us to prosperity. And as that process plays out, and the Fed’s balance sheet grows ridiculously large, credibility will inevitably be lost as the impotence of the QE program is revealed. Gold should do well in such an environment.

-An interesting thought experiment on what a Chinese move to peg the dollar (not the yuan) to a gold standard could look like.

(All articles come courtesy of Ed Steers’ daily email.)

-Next up is an article from the RT website that details how the U.S. has busted through the debt limit ahead of schedule. So far, it has not gotten much attention. As an aside, one interesting forecast in the Stockman book was premised on the notion that the U.S. no longer has a real appetite for large increases in the outstanding debt load. Thus, the “fiscal cliff” silliness of last year is set to become a recurring soap opera, with politicians always trying to do just enough to keep the ball moving. However, it stands to reason that the impact will be deflationary, with consumers trying to re-trench and saving more in the face of a slowing economy. Thus, we will probably see even more depressing GDP prints over time, even as the Fed tries to print us to prosperity. And as that process plays out, and the Fed’s balance sheet grows ridiculously large, credibility will inevitably be lost as the impotence of the QE program is revealed. Gold should do well in such an environment.

-An interesting thought experiment on what a Chinese move to peg the dollar (not the yuan) to a gold standard could look like.

(All articles come courtesy of Ed Steers’ daily email.)

Monday, July 29, 2013

The Great Deformation

The subtitle is The Corruption of Capitalism in America and the author is David Stockman (2013).

For those who don’t remember its release earlier this year, the book was received with much criticism from economists, politicians and media members alike, of all stripes. Having read it, I think I get it now.

His 700-plus page tome is nothing if not a scathing criticism of the Federal Reserve, liberals, conservatives, and anyone else who has contributed to a deformation of the free market system. The tipping point in the book is August, 1971, when Nixon severed the dollar’s ties to gold; however, Stockman considers other impactful moments that came before and after.

From a conduct standpoint, the main villain is the Fed. Particularly under Greenspan, that institution has become too focused on, and got into the business of, propping up the stock market, creating a gambler’s paradise where the pricing of financial assets often has no correlation to the underlying earnings and fundamentals. It is all about the “wealth effect” sponsored by the carry trade, with big banks and hedge fund punters trying to front-run any Fed move, with the Fed always there to give away money at the first sign of distress. So, in the aftermath of the 2008/2009 downturn, the stock market has ramped up 150%, but other economic data points don’t seem nearly as compelling – whether it’s retail sales, income growth, employment, debt/GDP ratios, etc.

Stockman levies criticisms at both parties, starting with the Republicans under Reagan. As you’ll recall, he was the budget director during the first term of that administration, but left and wrote a book about his disappointments with politics and politicians. Mainly, he is critical of the meme that got started in that period that deficits don’t matter, even though that story actually began pretty innocently. The idea behind the tax cuts under Reagan was to bring receipts as a percent of GDP back in-line with the Carter administration. But, the other assumptions built in, which included the idea that the Volcker fight with inflation would not bring a recession, were naïve with hindsight. At that point, the tax cuts became budget busters, but a recovering economy masked that fact in many respects (i.e., Volcker nipped inflation in the bud so P/E multiples expanded, with a natural recovery in earnings taking place anyway). Moreover, it was during that decade that the warfare state really got ramped up. Stockman shows a lot of respect for the Eisenhower administration, the only recent Presidency where a true military man was in charge, as it understood that the defense budget should be reduced with money efficiently targeted towards the nuclear deterrent – ground troops do nothing in the face of a Soviet strike. Of course, that wasn’t sustained post-Ike, and the defense budget has only grown bigger and bigger, often in the face of enemies both real and imagined. And both the tax and defense distortions were only multiplied during the presidency of George W. Bush and roundly endorsed by the Romney ticket in 2012.

Stockman does not hold back with the Democrats either, and for them he starts with the New Deal. In that period, perhaps with the best of intentions, certain of the big safety net programs saw their genesis – without any attending appreciation that all such programs are invariably captured by the special interests, because politicians are politicians in the end. And in the aftermath of Ike, you saw a shift in the Central Bankers, under the Democrats, to those who believed in the notion of a New Economics and the Phillips Curve – that there could be some master fiddler able to calibrate inflation and employment through monetary policy. Really, what we saw more than anything in the 1960s and 1970s was surging inflation. “Guns and butter” deficits turned into more warfare and welfare, with low rates and easy debt to reinforce the equation.

Of course, the pivotal moment was in 1971 with the move to a floating exchange rate. An entire industry of hedging sprouted up – never before had there been a need for a futures market in interest rates and bonds. Everything became commoditized and anything could be speculated on, with volatility ramping up relative to the past. Even worse, every cycle since 1971 has only upticked the level of credit in the system. To put a Hyman Minsky twist on it, with a lender of last resort, the prior inflation never went away.

In a truly free market with sound money, such excesses could not be sustained. As borrowing climbs, rates would climb as well, thus the engines are cooled. Yes, it can be recessionary, but it also gives cover to politicians to take the necessary steps to correct imbalances. We are without that now. Add to it, we have mercantilist economies in the East prepared to buy up our debt to sustain their export-based agendas. Americans can buy on credit without the need to save, the Central Bank can print up dollars at will to keep assets prices high, and thus the credit cycle can continue and we can extend and pretend. Point of fact, a state with the reserve currency is not supposed to run huge trade deficits and suck the capital out of other countries, while at the same time hollowing out its own manufacturing capacity since it can buy anything it wants without building up the capital first. The U.S. has become a nation of consumers with unsustainable balance sheets and with a Fed always looking to gin up financial asset prices.

So, to end where we started, the book was widely-blasted when it came out. But, having read it, I kind of think a lot of those critics didn’t read it, and only cherry-picked a particular data point to help discredit the whole thing. There is simply too much evidence of crony capitalism and terrible central planning from the monetary politburo, with a healthy side dish of bought and paid for politicians, to conclude anything else but that we are on an unsustainable path. Of course, in this day and age, most people are programmed to accept what they are told by the political overlords. And that’s why there is trouble down the road, perhaps worse than the last time.

For those who don’t remember its release earlier this year, the book was received with much criticism from economists, politicians and media members alike, of all stripes. Having read it, I think I get it now.

His 700-plus page tome is nothing if not a scathing criticism of the Federal Reserve, liberals, conservatives, and anyone else who has contributed to a deformation of the free market system. The tipping point in the book is August, 1971, when Nixon severed the dollar’s ties to gold; however, Stockman considers other impactful moments that came before and after.

From a conduct standpoint, the main villain is the Fed. Particularly under Greenspan, that institution has become too focused on, and got into the business of, propping up the stock market, creating a gambler’s paradise where the pricing of financial assets often has no correlation to the underlying earnings and fundamentals. It is all about the “wealth effect” sponsored by the carry trade, with big banks and hedge fund punters trying to front-run any Fed move, with the Fed always there to give away money at the first sign of distress. So, in the aftermath of the 2008/2009 downturn, the stock market has ramped up 150%, but other economic data points don’t seem nearly as compelling – whether it’s retail sales, income growth, employment, debt/GDP ratios, etc.

Stockman levies criticisms at both parties, starting with the Republicans under Reagan. As you’ll recall, he was the budget director during the first term of that administration, but left and wrote a book about his disappointments with politics and politicians. Mainly, he is critical of the meme that got started in that period that deficits don’t matter, even though that story actually began pretty innocently. The idea behind the tax cuts under Reagan was to bring receipts as a percent of GDP back in-line with the Carter administration. But, the other assumptions built in, which included the idea that the Volcker fight with inflation would not bring a recession, were naïve with hindsight. At that point, the tax cuts became budget busters, but a recovering economy masked that fact in many respects (i.e., Volcker nipped inflation in the bud so P/E multiples expanded, with a natural recovery in earnings taking place anyway). Moreover, it was during that decade that the warfare state really got ramped up. Stockman shows a lot of respect for the Eisenhower administration, the only recent Presidency where a true military man was in charge, as it understood that the defense budget should be reduced with money efficiently targeted towards the nuclear deterrent – ground troops do nothing in the face of a Soviet strike. Of course, that wasn’t sustained post-Ike, and the defense budget has only grown bigger and bigger, often in the face of enemies both real and imagined. And both the tax and defense distortions were only multiplied during the presidency of George W. Bush and roundly endorsed by the Romney ticket in 2012.

Stockman does not hold back with the Democrats either, and for them he starts with the New Deal. In that period, perhaps with the best of intentions, certain of the big safety net programs saw their genesis – without any attending appreciation that all such programs are invariably captured by the special interests, because politicians are politicians in the end. And in the aftermath of Ike, you saw a shift in the Central Bankers, under the Democrats, to those who believed in the notion of a New Economics and the Phillips Curve – that there could be some master fiddler able to calibrate inflation and employment through monetary policy. Really, what we saw more than anything in the 1960s and 1970s was surging inflation. “Guns and butter” deficits turned into more warfare and welfare, with low rates and easy debt to reinforce the equation.

Of course, the pivotal moment was in 1971 with the move to a floating exchange rate. An entire industry of hedging sprouted up – never before had there been a need for a futures market in interest rates and bonds. Everything became commoditized and anything could be speculated on, with volatility ramping up relative to the past. Even worse, every cycle since 1971 has only upticked the level of credit in the system. To put a Hyman Minsky twist on it, with a lender of last resort, the prior inflation never went away.

In a truly free market with sound money, such excesses could not be sustained. As borrowing climbs, rates would climb as well, thus the engines are cooled. Yes, it can be recessionary, but it also gives cover to politicians to take the necessary steps to correct imbalances. We are without that now. Add to it, we have mercantilist economies in the East prepared to buy up our debt to sustain their export-based agendas. Americans can buy on credit without the need to save, the Central Bank can print up dollars at will to keep assets prices high, and thus the credit cycle can continue and we can extend and pretend. Point of fact, a state with the reserve currency is not supposed to run huge trade deficits and suck the capital out of other countries, while at the same time hollowing out its own manufacturing capacity since it can buy anything it wants without building up the capital first. The U.S. has become a nation of consumers with unsustainable balance sheets and with a Fed always looking to gin up financial asset prices.

So, to end where we started, the book was widely-blasted when it came out. But, having read it, I kind of think a lot of those critics didn’t read it, and only cherry-picked a particular data point to help discredit the whole thing. There is simply too much evidence of crony capitalism and terrible central planning from the monetary politburo, with a healthy side dish of bought and paid for politicians, to conclude anything else but that we are on an unsustainable path. Of course, in this day and age, most people are programmed to accept what they are told by the political overlords. And that’s why there is trouble down the road, perhaps worse than the last time.

Friday, July 26, 2013

Free Markets at last?

I have been paying attention over recent months to the quickly declining eligible gold holdings in Comex vaults for JP Morgan and other bullion banks (all of which suggested the possibility that the day of reckoning was approaching for the paper market). Add to that, there has been some media focus this past week to the idea of manipulation by financial institutions in the commodity space, such as with aluminum. So, like Zero Hedge, consider me less than shocked then that JP Morgan has decided to exit the physical commodity business…

Charts and Stuff

-Despite not saying much recently, I never stopped paying attention to the Yen. The chart (shown below) looks to be completing a head-and-shoulders formation. To be more specific, the left shoulder tracks from February to early April of this year, the head goes from early April to mid-June, and the right shoulder has been forming since then, and now appears to be closer to its conclusion than its inception. Incrementally, it has to break below 98, then 97, then 94.5 to confirm the move. If it does all of that, the target would be somewhere back in the mid-80s yen to the dollar. And that would not be according to the script for Abenomics – because as has been pointed out by several very smart folks (including Kyle Bass), the 2% inflation target will require an exchange rate closer to 120.

-An article that delves into the recidivism prevalent in the government’s foreclosure prevention program. A highlight: “The Home Affordable Modification Program (HAMP) has worked on 1.2 million mortgage modifications since it started four years ago. Of those, more than 306,000 borrowers have defaulted again on their loans, and another 88,000 are at risk as well.”

-An article that delves into the recidivism prevalent in the government’s foreclosure prevention program. A highlight: “The Home Affordable Modification Program (HAMP) has worked on 1.2 million mortgage modifications since it started four years ago. Of those, more than 306,000 borrowers have defaulted again on their loans, and another 88,000 are at risk as well.”

Thursday, July 25, 2013

Smart Read of the Day

Today brings us the most recent commentary from Doug Noland at The Prudent Bear website. Below is an interesting excerpt:

“For me, the primary focus on Credit always resonated. An expansion of debt – “Credit inflation” – will have consequences, although the nature of the inflationary effects can differ greatly depending on the nature of the underlying Credit expansion, the particular prevailing flow of the new purchasing power and, importantly, the structure of the real economy (domestic and global). The increase in purchasing power may or may not increase a general measure of consumer prices. It might be directed to imports and inflate trade and Current Account deficits. It may fuel investment. Or it could flow into housing and securities markets – perhaps inflating asset Bubbles.

Dr. Richebacher persuasively argued that rising consumer price inflation was the least problematic inflationary manifestation, as it could be rectified by determined (Volcker-style) monetary tightening. Presciently, Richebacher viewed asset inflation and Bubbles as the much more dangerous inflationary strain – too easily tolerated, accommodated or even propagated.

It’s no coincidence that periods of low consumer price inflation preceded the Great Depression and the bursting of the Japanese Bubble. I would further note that consumer price inflation was relatively contained prior to the bursting of the tech and mortgage finance Bubbles. But to claim this dynamic was caused by tight monetary policy is flawed thinking. It was just the opposite.”

“For me, the primary focus on Credit always resonated. An expansion of debt – “Credit inflation” – will have consequences, although the nature of the inflationary effects can differ greatly depending on the nature of the underlying Credit expansion, the particular prevailing flow of the new purchasing power and, importantly, the structure of the real economy (domestic and global). The increase in purchasing power may or may not increase a general measure of consumer prices. It might be directed to imports and inflate trade and Current Account deficits. It may fuel investment. Or it could flow into housing and securities markets – perhaps inflating asset Bubbles.

Dr. Richebacher persuasively argued that rising consumer price inflation was the least problematic inflationary manifestation, as it could be rectified by determined (Volcker-style) monetary tightening. Presciently, Richebacher viewed asset inflation and Bubbles as the much more dangerous inflationary strain – too easily tolerated, accommodated or even propagated.

It’s no coincidence that periods of low consumer price inflation preceded the Great Depression and the bursting of the Japanese Bubble. I would further note that consumer price inflation was relatively contained prior to the bursting of the tech and mortgage finance Bubbles. But to claim this dynamic was caused by tight monetary policy is flawed thinking. It was just the opposite.”

Thursday, July 18, 2013

(Another) Quote of the Day

Another gem from Michael E. Lewitt, this time in his July, 2013 newsletter:

“The policies that are being employed to create the appearance of economic and market stability are not effectively addressing the underlying symptoms of economic malaise; in fact, they are exacerbating them. Debt is being used to cure a debt crisis in the hope that fiscal policies will be implemented that will foment sufficiently high economic growth to create the income necessary to service and ultimately repay that debt. But even in the best of all possible worlds such an outcome would be a long shot since the sheer amount of debt being generated to keep economies afloat is too large to be serviced or repaid. And as we are all painfully aware, we don’t live in the best of all possible worlds – we live in a world populated by corrupt and narcissistic politicians and business leaders who refuse to effect the necessary fiscal reforms that would at least give monetary policy a chance to work. As a result, the post-crisis world has been left more indebted and more interconnected than the pre-crisis world. The tails may be buried a little deeper than they were, but they are fatter than ever.”

“The policies that are being employed to create the appearance of economic and market stability are not effectively addressing the underlying symptoms of economic malaise; in fact, they are exacerbating them. Debt is being used to cure a debt crisis in the hope that fiscal policies will be implemented that will foment sufficiently high economic growth to create the income necessary to service and ultimately repay that debt. But even in the best of all possible worlds such an outcome would be a long shot since the sheer amount of debt being generated to keep economies afloat is too large to be serviced or repaid. And as we are all painfully aware, we don’t live in the best of all possible worlds – we live in a world populated by corrupt and narcissistic politicians and business leaders who refuse to effect the necessary fiscal reforms that would at least give monetary policy a chance to work. As a result, the post-crisis world has been left more indebted and more interconnected than the pre-crisis world. The tails may be buried a little deeper than they were, but they are fatter than ever.”

The Pending Health Care Problem

A really interesting guest piece on the Casey Research site yesterday...

Hidden Consequences of the Employer Mandate Delay

Obamacare is a hodgepodge of new regulations, requirements, and penalties. I'd like to start by defining three terms which, while obscure today, should begin to enter our everyday vocabulary as Obamacare continues to take effect:

Health insurance exchanges are the basket of qualified insurance policies that meet the new healthcare law requirements for expanded coverage. These may be set up by the states (many are refusing to do so, due to high cost and fear of bankrupting the state) or the federal government. The Exchanges are supposed to be fully operational by October 1, 2013, but it is questionable whether they will actually be in place by that deadline.

The individual mandate requires that individuals purchase health insurance that meets the new, expanded federal requirements. Individuals who do not comply face a financial penalty. Individuals who fall below minimum income levels will be eligible for taxpayer-funded subsidies to buy health insurance.

The employer mandate requires that businesses with more than 50 fulltime employees must provide health insurance for all employees, and that insurance must meet the new standards set forth in the new law. Businesses that do not comply must pay a financial penalty for each employee, which for large companies can run into the millions of dollars annually. This is the piece of Obamacare that has been delayed by one year.

To answer that question, we must first understand this fact: Obama wants a single-payer healthcare system in the US. This is not a secret:

These quotes are not taken out of context. Anyone who has been paying attention knows that transitioning to a single-payer system has been Obama's and his cohorts' ultimate goal all along:

Here, Rep. Schakowsky is suggesting that the "public option" will lead to their desired goal of a single-payer healthcare system. Single-payer proponents no longer use this term, since the public has clearly and consistently opposed it. The "public option" has been renamed "Medicaid expansion," which serves the public-relations purpose of confusing the public and avoiding calling taxpayer-funded healthcare "single payer."

Hacker nicely sums up the underlying goals of Obamacare: not to increase competition or patient choice, but to drive people out of private insurance as a stepping stone to a government-run, single-payer system.

By forcing individuals to purchase compliant healthcare plans but not forcing employers to provide those plans, Obama is creating a swell of 10-13 million workers that must enroll in health insurance, but cannot obtain it from their employers. These workers thus have no choice but to use the government-controlled health insurance exchanges, or else pay a financial penalty. This represents a doubling of the number of workers forced to get health insurance on the exchanges.

Importantly, the IRS has ruled that if workers have access to affordable health insurance through their employer, their dependents are not eligible for taxpayer-funded subsidies on the Obamacare health insurance exchanges. Now that businesses will not be required to offer health insurance until 2015, workers and their dependents will be eligible for taxpayer-funded subsidies to purchase health insurance on the exchanges. This will cost taxpayers an estimated $60 billion dollars in 2014 alone to cover the increased costs of subsidies—and the loss of revenue from employer penalties.

This $60-billion figure is before we take into account the "liar subsidies" that will invariably occur now that the Administration has quietly removed eligibility verification for taxpayer-funded subsidies. Community organizers are already being hired around the country to sign people up for the health exchanges. There are no penalties for failing to verify eligibility, and no penalties for signing up people who cannot afford to pay the monthly insurance premiums. It is set up for disaster, much like the "liar loans" that helped topple the mortgage industry when people were not required to verify their income to qualify for a mortgage.

Remember, by enacting the dual mandates, Obamacare ostensibly was designed to ensure that its costs were borne by businesses, not taxpayers. But when the president decided to enforce only certain portions of the healthcare law and delay others, he shifted the cost of health insurance onto the backs of taxpayers.

This is all on top of the burdensome costs Obamacare has already created. Various studies have projected that private insurance premiums will rise between 20 to 60% in 2014, and some as much as 100%.

How long will the private-insurance market survive with such exploding costs? People will not be able to afford such massive premium increases. That seems to be the point: drive up costs and drive everyone into the arms of government-controlled medical care.

Jeff Smith from Seattle summed it up nicely in a Wall Street Journal letter on June 12:

Americans need to become far more proactive about taking charge of their health. The healthier you are, the less vulnerable you are to our degrading healthcare system. It's also wise to consider proactively planning for medical treatment options outside the US.

Hidden Consequences of the Employer Mandate Delay

By Elizabeth Lee Vliet, M.D.

Obamacare is a hodgepodge of new regulations, requirements, and penalties. I'd like to start by defining three terms which, while obscure today, should begin to enter our everyday vocabulary as Obamacare continues to take effect:

Health insurance exchanges are the basket of qualified insurance policies that meet the new healthcare law requirements for expanded coverage. These may be set up by the states (many are refusing to do so, due to high cost and fear of bankrupting the state) or the federal government. The Exchanges are supposed to be fully operational by October 1, 2013, but it is questionable whether they will actually be in place by that deadline.

The individual mandate requires that individuals purchase health insurance that meets the new, expanded federal requirements. Individuals who do not comply face a financial penalty. Individuals who fall below minimum income levels will be eligible for taxpayer-funded subsidies to buy health insurance.

The employer mandate requires that businesses with more than 50 fulltime employees must provide health insurance for all employees, and that insurance must meet the new standards set forth in the new law. Businesses that do not comply must pay a financial penalty for each employee, which for large companies can run into the millions of dollars annually. This is the piece of Obamacare that has been delayed by one year.

Selective Enforcement

Why delay one component of Obamacare and not the others? More specifically, why delay the employer mandate but not the individual mandate?To answer that question, we must first understand this fact: Obama wants a single-payer healthcare system in the US. This is not a secret:

Barrack Obama, 2003: "I happen to be a proponent of a single-payer healthcare system for America, but as all of you know, we may not get there immediately."

Barrack Obama, 2007: "But I don't think we will be able to eliminate employer-based coverage immediately. There is potentially going to be some transition time."

Rep Jan Schakowsky (D-IL), 2009: "Next to me was a guy from the insurance company who then argued against the public option. He said it would not let private insurance companies compete. A public option would put the private insurance companies out of business and lead to single-payer. My single payer friends, he was right. The man was right!"

Jacob S. Hacker (Yale Professor), 2008: "Someone once said to me this is a Trojan Horse for single payer. It's not a Trojan Horse, right? It's right there! I am telling you. We are going to get there. Over time. Slowly. But we are going to move away from reliance on employer-based health insurance, as we should, but we will do it in a way that we are not going to frighten people into thinking they are going to lose their private insurance. We will give them a choice of public or private insurance when they are in the pool. We are going to let them keep their private insurance as long as their employer continues to provide it."

Stepping Stone to Single-Payer

Knowing Obama and his cohorts' goals, the purpose behind the delay of the employer mandate seems clearer: to hurry the "transition time" away from employer-based health insurance and to a single-payer system.By forcing individuals to purchase compliant healthcare plans but not forcing employers to provide those plans, Obama is creating a swell of 10-13 million workers that must enroll in health insurance, but cannot obtain it from their employers. These workers thus have no choice but to use the government-controlled health insurance exchanges, or else pay a financial penalty. This represents a doubling of the number of workers forced to get health insurance on the exchanges.

Importantly, the IRS has ruled that if workers have access to affordable health insurance through their employer, their dependents are not eligible for taxpayer-funded subsidies on the Obamacare health insurance exchanges. Now that businesses will not be required to offer health insurance until 2015, workers and their dependents will be eligible for taxpayer-funded subsidies to purchase health insurance on the exchanges. This will cost taxpayers an estimated $60 billion dollars in 2014 alone to cover the increased costs of subsidies—and the loss of revenue from employer penalties.

This $60-billion figure is before we take into account the "liar subsidies" that will invariably occur now that the Administration has quietly removed eligibility verification for taxpayer-funded subsidies. Community organizers are already being hired around the country to sign people up for the health exchanges. There are no penalties for failing to verify eligibility, and no penalties for signing up people who cannot afford to pay the monthly insurance premiums. It is set up for disaster, much like the "liar loans" that helped topple the mortgage industry when people were not required to verify their income to qualify for a mortgage.

Remember, by enacting the dual mandates, Obamacare ostensibly was designed to ensure that its costs were borne by businesses, not taxpayers. But when the president decided to enforce only certain portions of the healthcare law and delay others, he shifted the cost of health insurance onto the backs of taxpayers.

This is all on top of the burdensome costs Obamacare has already created. Various studies have projected that private insurance premiums will rise between 20 to 60% in 2014, and some as much as 100%.

How long will the private-insurance market survive with such exploding costs? People will not be able to afford such massive premium increases. That seems to be the point: drive up costs and drive everyone into the arms of government-controlled medical care.

Jeff Smith from Seattle summed it up nicely in a Wall Street Journal letter on June 12:

"I was going to leave my job…to start a business until I shopped around for a healthcare plan: At Group Health, a health-maintenance organization in Seattle, I was given a quote of $842 per month for me and my family. But that would increase to $2,320 starting in January 2014 when Obamacare kicks in—a 276% increase. Why? Because I would be forced to carry coverage I don't want and don't need, such as maternity care. Welcome to the world of socialized medicine, courtesy of the Un-Affordable Care Act."

How Obamacare Affects You and Your Medical Care

The delay in the employer mandate is but one of dozens of negative impacts Obamacare will have on your medical services. As an independent physician, I've been discussing these issues with my patients for the past few years, helping them to prepare for what's ahead. Here the ten most important points that I tell my patients:- Your private insurance premiums will cost more and more each year.

- You will lose the choices and flexibility in health insurance policies that we have had available up until now.

- As reimbursements continue to drop, fewer and fewer doctors will take Medicare (for those 65 and older) or Medicaid (people younger than 65).

- Fewer doctors accepting Medicare and Medicaid causes an increase in wait times for appointments and a decrease in the numbers and types of specialists available on these plans. Consumers would be wise to line up their doctors now.

- Studies from various organizations and states have consistently shown that Medicaid recipients have longer waits for medical care, fewer options for specialists, poorer medical outcomes, and die sooner after surgeries than people with no health insurance at all. Yet an increasing number of Americans will be forced into this second-class medical care.

- As more people enter the taxpayer-funded plans (Medicare and Medicaid) instead of paying for private insurance, the costs to provide this increased medical care and medications will escalate, leading to higher taxes.

- With no eligibility verifications in place, millions of people who are in the US illegally will be able to access taxpayer-funded medical services, making longer lines, longer wait times, and less money available for medical care for American citizens… unless taxes are increased even more.

- Higher expenditures to provide medical services lead to rationing of medical care and treatment options to reduce costs. This is the mandated function of the Independent Payment Advisory Board: to cut costs by deciding which types of medical services to allow… or disallow. If you are denied treatment, you have no appeal of IPAB decisions; you are simply out of luck, and possibly out of life. This is a radical departure from the appeals process required for all private health insurance plans. Further, the IPAB is accountable only to President Obama, and cannot be overridden by Congress or the courts. IPAB is designed to have the final word on your health.

- Under current regulations, if medical care is denied by Medicare, then a patient is not allowed to pay cash to a Medicare-contracted physician or hospital or other health professional. Patients who need medical care that is denied under Medicare or Medicaid will find themselves having to either: 1) look for an independent physician or hospital (quite rare these days); or 2) go outside the USA for treatment.

- Expect a loss of medical privacy. Beginning in 2014, if you participate in government health insurance, your health records will be sent to a centralized federal database, with or without your consent.

Americans need to become far more proactive about taking charge of their health. The healthier you are, the less vulnerable you are to our degrading healthcare system. It's also wise to consider proactively planning for medical treatment options outside the US.

Quote(s) of the Day

A couple from Michael E. Lewitt who writes the really interesting monthly newsletter The Credit Strategist. Both are from the June, 2013 issue. The first, I think, does a great job of capturing the idea that I have often struggled to convey in my posts. The second offers some perspective on just how vulnerable many investors are right now with inevitability of higher rates, not to mention the companies that will suddenly confront much higher interest expenses against stagnating earnings.

“This lack of conviction in the ability of stocks to maintain current levels without the continued support of the Federal Reserve also suggests that investors remain suspicious of the veneer of market stability that monetary policy has created.”

“Recent work by Charles Gave, chairman of GaveKal Research, showed that of the world’s roughly $209 trillion of financial assets, $45 trillion is invested in government debt, $65 trillion is in loans, and $46 trillion is in corporate debt. That means that a total of $156 trillion, or 75% of the total, is invested in assets that are likely to produce negative real returns over the next five years (and probably longer).”

“This lack of conviction in the ability of stocks to maintain current levels without the continued support of the Federal Reserve also suggests that investors remain suspicious of the veneer of market stability that monetary policy has created.”

“Recent work by Charles Gave, chairman of GaveKal Research, showed that of the world’s roughly $209 trillion of financial assets, $45 trillion is invested in government debt, $65 trillion is in loans, and $46 trillion is in corporate debt. That means that a total of $156 trillion, or 75% of the total, is invested in assets that are likely to produce negative real returns over the next five years (and probably longer).”

Liar's Poker

To read this book by Michael Lewis (1989) was a long time coming. It is about Wall Street in the ‘80s, primarily Salomon Brothers where he worked as a bonds salesman for a few years. The story really demonstrates that the antecedent for a lot of the recent reckless behavior can be traced to that era – from the growth of a mortgage bond market, to arguably unscrupulous behavior with clients’ money, to a culture driven by wealth and conspicuous consumption, to the careless use of leverage in trading.

I enjoyed his description of the trading floor, as I could never give a good answer before to the question of what people in sales & trading at the big banks do. You also get an insight into the key players at that firm, like John Gutfreund and Lewis Ranieri (who is often viewed as the architect of the mortgage bond market, whether intended or not).

The title of the book refers to a gambling game that traders would often partake in, making use of serial numbers on dollar bills (think of something similar to the card game “Bullshit”). The mentality, reasoning and behavior to succeed in that game often translated to success as a trader. And it also serves as a measure of the greed and ego that has always driven Wall Street.

I enjoyed his description of the trading floor, as I could never give a good answer before to the question of what people in sales & trading at the big banks do. You also get an insight into the key players at that firm, like John Gutfreund and Lewis Ranieri (who is often viewed as the architect of the mortgage bond market, whether intended or not).

The title of the book refers to a gambling game that traders would often partake in, making use of serial numbers on dollar bills (think of something similar to the card game “Bullshit”). The mentality, reasoning and behavior to succeed in that game often translated to success as a trader. And it also serves as a measure of the greed and ego that has always driven Wall Street.

Wednesday, July 17, 2013

New Short Position

I might be premature in making this assessment, but my view is that if the market is poised to break above 1687.18, then today with Bernanke's testimony would be the day. He basically said all the same things as last week, but the market stalled out (as of this writing) somewhere around 1682. And, so, I initiated a new short position on XLK (the technology ETF).

Better Conspiracy Theories

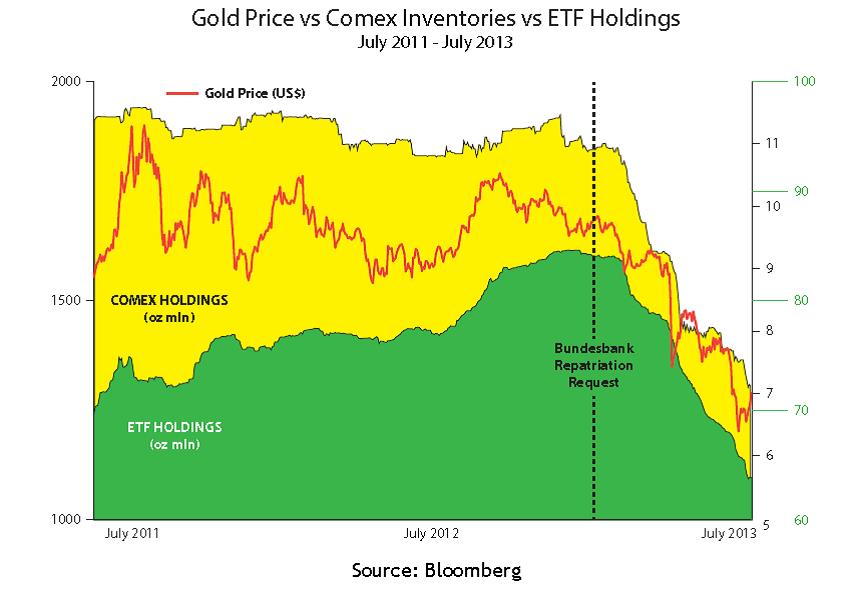

In Grant Williams’ most recent piece for Mauldin Economics, he offers up a decent case for how the dramatic moves in gold are very much tied up with requests by sovereign nations to take their gold out of the NY Federal Reserve bank vault and ship it home. He spends some time around the request by Venezuela in the fall of 2011 for 99 tonnes, but then spends a great deal more energy focused on the request earlier this year by the Bundesbank to retrieve 300 tonnes from New York and 347 tonnes from France. Oddly, it’s going take 7 years for the Germans to get their gold from the former and 5 years from the latter.

To tie it up, the theory is that the gold leasing program by Central Banks has led to gold that gets hypothecated and then re-hypothecated again. In other words, it’s basically gone, and with demand increasing for the physical stuff, bullion banks now must scramble and put on naked shorts to try and shake out weak hands and buy back ounces. Who knows. I would point out that Williams is not the first to make this case, but only the most recent. And better yet, he offers a really interesting chart that looks at price against the inventories at Comex and GLD since the German request.

The other bit of reading comes courtesy of Ben Hunt, an economist who provides a simply too-long and pretentious take on gold – that those who still view it as money have missed the paradigm shift. Rather, today it’s all about central bankers and their machinations. So, basically, this guy takes a lot of words to get to the same point that Jim Grant has long made in his simple equation of 1/T – the price of gold is the inverse of “T”, the amount of confidence that people have in the central planners.

To tie it up, the theory is that the gold leasing program by Central Banks has led to gold that gets hypothecated and then re-hypothecated again. In other words, it’s basically gone, and with demand increasing for the physical stuff, bullion banks now must scramble and put on naked shorts to try and shake out weak hands and buy back ounces. Who knows. I would point out that Williams is not the first to make this case, but only the most recent. And better yet, he offers a really interesting chart that looks at price against the inventories at Comex and GLD since the German request.

The other bit of reading comes courtesy of Ben Hunt, an economist who provides a simply too-long and pretentious take on gold – that those who still view it as money have missed the paradigm shift. Rather, today it’s all about central bankers and their machinations. So, basically, this guy takes a lot of words to get to the same point that Jim Grant has long made in his simple equation of 1/T – the price of gold is the inverse of “T”, the amount of confidence that people have in the central planners.

Tuesday, July 16, 2013

Quote of the Day

"They that can give up essential liberty to obtain a little temporary safety deserve neither liberty nor safety."

-Benjamin Franklin

-Benjamin Franklin

Thursday, July 11, 2013

Difference with a Distinction

I saw an interview today where Jim Rogers took the position that gold is in the midst of a complicated bottoming process that will probably take it down to somewhere between $900 and $1,000. Maybe he's right. At the same time, he is not selling and thinks that gold's bull market is far from over.

I contrast his view with others who think gold is headed lower, whether it's $900, $800 or $600 per ounce, but take that position on the premise that gold holds no merit. Rogers is able to contextualize and seems to get the bigger trends right -- these folks just don't like gold. And, unlike Rogers, should probably just be ignored.

I contrast his view with others who think gold is headed lower, whether it's $900, $800 or $600 per ounce, but take that position on the premise that gold holds no merit. Rogers is able to contextualize and seems to get the bigger trends right -- these folks just don't like gold. And, unlike Rogers, should probably just be ignored.

Foot still in mouth

More bullish signs for gold:

-For a change, Au responded the way you would have expected with Bernanke making clear that money-printing ad infinitum is the once and future strategy

-The GOFO has been negative for several days in a row now. The short explanation is that the Gold Forward rate (GOFO) is used in gold-dollar swaps, where people who need dollars can put up gold as collateral and pay a low interest rate to borrow. A negative rate implies that the demand is now in the opposite direction – people are prepared to put up dollars as collateral and pay interest to get their hands on the physical stuff. It would appear that all the stories of surging physical demand in the East and dealers/exchanges running out of supply are in fact true.

-As discussed yesterday, and although only for a short-term projection, the chart is becoming a bit more constructive. And you can see it across the mining shares as well.

Don’t get me wrong, I am still cautious about the near-term and tend to think that down is still the path of least resistance. But changes like those listed above are all part of a bottoming process.

-For a change, Au responded the way you would have expected with Bernanke making clear that money-printing ad infinitum is the once and future strategy

-The GOFO has been negative for several days in a row now. The short explanation is that the Gold Forward rate (GOFO) is used in gold-dollar swaps, where people who need dollars can put up gold as collateral and pay a low interest rate to borrow. A negative rate implies that the demand is now in the opposite direction – people are prepared to put up dollars as collateral and pay interest to get their hands on the physical stuff. It would appear that all the stories of surging physical demand in the East and dealers/exchanges running out of supply are in fact true.

-As discussed yesterday, and although only for a short-term projection, the chart is becoming a bit more constructive. And you can see it across the mining shares as well.

Don’t get me wrong, I am still cautious about the near-term and tend to think that down is still the path of least resistance. But changes like those listed above are all part of a bottoming process.

Wednesday, July 10, 2013

Pulse of the Market

After the market closed, the Bernank spoke and was extra dovish. The upshot is that most asset classes have rallied, in particular the stock market where the futures currently put us back above 1660.

As you may recall, back in May I quoted John Hussman, who noted that at important market peaks (think 1929, 1987, 2007), what often happens is that there is a relatively quick 6% to 10% puke, followed by a move back up that quells concerns and suggests that everything is a-okay again, but without actually making a new high.

What have we seen?

On 5/22 the S&P 500 peaked at 1687.18, and over the next four weeks we saw an 8% correction down to 1560.33. Subsequently, the market has been fighting, gaining back roughly 80% of the ground that was lost (as of this writing).

So far, the Hussman roadmap is playing out pretty well. Obviously what we’re watching for though is whether the May high holds.

As you may recall, back in May I quoted John Hussman, who noted that at important market peaks (think 1929, 1987, 2007), what often happens is that there is a relatively quick 6% to 10% puke, followed by a move back up that quells concerns and suggests that everything is a-okay again, but without actually making a new high.

What have we seen?

On 5/22 the S&P 500 peaked at 1687.18, and over the next four weeks we saw an 8% correction down to 1560.33. Subsequently, the market has been fighting, gaining back roughly 80% of the ground that was lost (as of this writing).

So far, the Hussman roadmap is playing out pretty well. Obviously what we’re watching for though is whether the May high holds.

Foot In Mouth Disease

Maybe I’m a glutton for punishment – because I'm about to opine on the chart for gold and mining stocks again. And what I see in both the metal and a group of miners that I follow is a bullish cup and handle (i.e., the inverse of what I saw in GLD last month before it collapsed) which would suggest a decent move up. For gold, it’s probably good for at least $80 (and potentially a bit more).

And even if I didn’t see it, I would still argue that there is a big gap in the GLD chart (from 6/20/13) that needs to be closed before the next downswing should start. That gap is not closed until $130.38 gets hit, or about $85 bucks higher from here in the spot price. That fits a bit too perfectly.

And even if I didn’t see it, I would still argue that there is a big gap in the GLD chart (from 6/20/13) that needs to be closed before the next downswing should start. That gap is not closed until $130.38 gets hit, or about $85 bucks higher from here in the spot price. That fits a bit too perfectly.

Fundamentals?

I came across this really interesting chart regarding 2013 and 2014 EPS forecasts by region and globally. Note the very pronounced move from upper left to lower right. Which strikes me as a bad thing. Then, in your head, contrast it with the typical stock chart. If you're having trouble, the basic gist is a move from lower left to upper right -- going up. Is that how it should be? (Consider that last bit to be rhetorical.)

To further contextualize it for you, Alcoa recently "beat" street estimates by showing EPS of $0.07 this quarter instead of $0.06. But, bear in mind, the forecast has steadily been going down over time. Last year it was $0.30. Last month it was $0.10.

Draw your own conclusions.

To further contextualize it for you, Alcoa recently "beat" street estimates by showing EPS of $0.07 this quarter instead of $0.06. But, bear in mind, the forecast has steadily been going down over time. Last year it was $0.30. Last month it was $0.10.

Draw your own conclusions.

Monday, July 8, 2013

Peeling Back The Onion

A quick note about Friday’s jobs report, which showed 195,000 jobs added in the U.S. during the month of June. I think there’s only one thing worth focusing on – the household survey reported that part-time jobs increased by 360,000 while full-time jobs decreased by 240,000. Quite the divergence. Land of the free and home of the marginally employed. Did someone mention recovery?

(h/t Zero Hedge)

(h/t Zero Hedge)

Thursday, July 4, 2013

More Money Than God

My most recent read comes from Sebastian Mallaby (2010) and provides a history of the hedge fund industry, starting with Alfred Winslow Jones and working towards some of the prominent players from today.

The book highlights how the success of the hedgies, in their ability to generate alpha, undermines the theory of an efficient market, in that many investors only gradually adapt to new information, allowing for a small subset to really profit. At the same time, emotion and sentiment are powerful forces and can drive a trend much further than the fundamentals warrant. Therefore, the "art of speculation is to develop one insight that others have overlooked and then trade big on that small advantage", with the other key being an ability to identify the trigger point that will cause the pricing anomaly to correct and to move towards some fundamental equilibrium. Because, after all, to be right but early can often have the same feeling as being wrong.

Some of the big examples that capture that theme in the book are the Soros/Druckenmiller short of the British Pound (with lots of interesting detail on the genesis of the idea and its execution), the Paulson short of subprime, and the Paul Tudor Jones short of the market in 1987. As you may have picked up, it is often from the short side that the biggest wins are realized.

The book highlights how the success of the hedgies, in their ability to generate alpha, undermines the theory of an efficient market, in that many investors only gradually adapt to new information, allowing for a small subset to really profit. At the same time, emotion and sentiment are powerful forces and can drive a trend much further than the fundamentals warrant. Therefore, the "art of speculation is to develop one insight that others have overlooked and then trade big on that small advantage", with the other key being an ability to identify the trigger point that will cause the pricing anomaly to correct and to move towards some fundamental equilibrium. Because, after all, to be right but early can often have the same feeling as being wrong.

Some of the big examples that capture that theme in the book are the Soros/Druckenmiller short of the British Pound (with lots of interesting detail on the genesis of the idea and its execution), the Paulson short of subprime, and the Paul Tudor Jones short of the market in 1987. As you may have picked up, it is often from the short side that the biggest wins are realized.

Wednesday, July 3, 2013

Is Gold Money?

It sure sounds like the U.S. government thinks so.

This NY Times article from Monday documents the new sanctions against Iran that have taken effect, essentially banning anyone from selling or transferring gold to the country. As you have probably heard, to evade earlier sanctions, countries had been paying Iran for its fossil fuels with the barbarous relic. Thus, these new sanctions sure do seem like a tacit acknowledgement of gold’s role as a currency. And anytime you implement a capital control of this sort, the effect is commonly to increase the demand and price of said item. But we shall see.

This NY Times article from Monday documents the new sanctions against Iran that have taken effect, essentially banning anyone from selling or transferring gold to the country. As you have probably heard, to evade earlier sanctions, countries had been paying Iran for its fossil fuels with the barbarous relic. Thus, these new sanctions sure do seem like a tacit acknowledgement of gold’s role as a currency. And anytime you implement a capital control of this sort, the effect is commonly to increase the demand and price of said item. But we shall see.

Monday, July 1, 2013

Subscribe to:

Comments (Atom)

-

Are when the contrarian should think about buying. And so I tried. Some AUY LEAPS (filled) and a small mining services company that I like...

-

Lately, in spite of various frustrations, I have been trying to think through where the opportunities will be in real estate. We’ve discuss...

-

I came across this really interesting chart regarding 2013 and 2014 EPS forecasts by region and globally. Note the very pronounced move fr...

I came across this really interesting chart regarding 2013 and 2014 EPS forecasts by region and globally. Note the very pronounced move fr...