The subtitle is

The Coming Collapse of the International Monetary System and the author is James Rickards (2014).

From the same writer as

Currency Wars, the subtitle should give it away – he looks at the dynamics at play that will undermine the existing structure, specifically dollar supremacy. All of it presages financial war, a state where efficient markets theory and rational behavior can be thrown out the window. Unfortunately, politicians, central bankers and the like rely on theories and models that in no way reflect the complexity theory that governs the real world – in part, because a complex world can seem noncritical up until the moment that all hell breaks loose. Hence the reason that so many “experts” struggle to see crises in advance. And this sense of confidence in their understanding of the world is what encourages these central planners to take a top-down approach of managing and fine-tuning all elements of the economy. All leading to their eventual downfall. Beyond these larger ideas, though, Rickards provides interesting analysis on a few specific topics.

The first is an explanation of why so many “Euroskeptics”, expecting the currency to combust any day now, have been wrong. First, in a world where the U.S. has been forcing a weak dollar policy, it should not come as a shock that the Euro would gain relative strength. Second, the currency’s strength is more related to capital flows and central bank policy, and is not at the mercy of a particular bond default – so the issues with Greek and Spanish bonds does not predict with any certainty what might happen to the Euro. Third, even as export competitiveness went down in Europe, the U.S. and China were involved in swaps with the ECB and sending money into Europe in the form of FDI, thereby supporting the currency. Fourth, there exists a belief in Keynesian theory, specifically in the notion of sticky wages and that inflation is needed to lower real unit labor costs and to avoid a liquidity trap. Well, Europe has seen wages go down, and the result has been a lack of need or desire to break free from the Euro and return to national currencies that encouraged inflation and corruption. Finally, as the Euro is a political project, the will to stick with it is much greater than many analysts realize. I don’t necessarily subscribe to all these points, but feel they are worth highlighting.

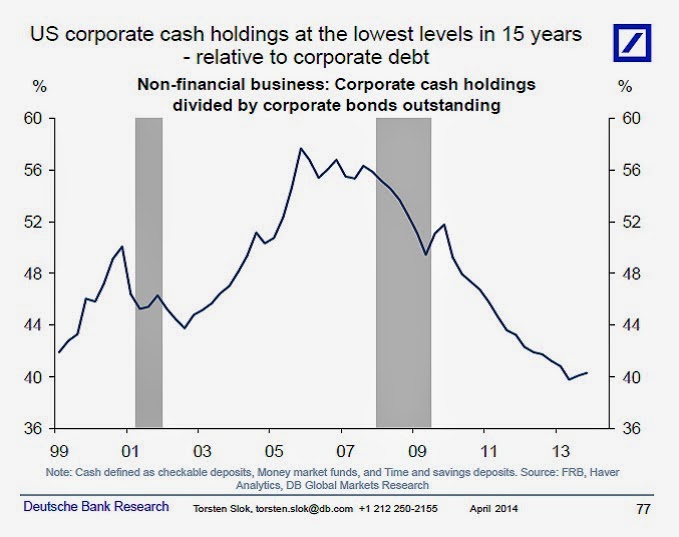

The second subject is the way to think about Debt-to-GDP ratios. In the end, what is most critical is not the absolute level of that ratio, but its trend towards sustainability. Which is to say that the use of debt must be for productive ends, thereby creating economic output (net of interest expense) that is measurably in excess of the primary deficit. For countries like the U.S. and Japan, the trend is not their friend – especially as the use of debt by government in the QE and Abenomics programs is for non-productive ends.

As a corollary of that discussion, Rickards brings up a topic that has intrigued me for a while and generated thoughts in other posts on this site – namely, about a true understanding of the period referred to as the “Golden Age of Keynesianism” following WW2 until 1971. I have said that a Minsky analysis of that time would reveal, simply, that the trend towards reckless and speculative behavior was slowed only because the Depression and war had led to a very high level of savings in this country that took a longer time to burn through – the Keynesians simply try to take credit where no credit is due. Rickards’ view is similar – that financial repression was allowed to go on for a longer period of time before inflation took off because so many were living with recent memories of the Depression and wartime controls and rationing, thus keeping a very large portion of their money in banks.

The final topic is around why deflation is so problematic – from the point of view of politicians and central bankers. First, under deflation, the government debt burden becomes greater in real terms, making it more difficult to repay. Second, as an off-shoot of the first, the Debt-to-GDP ratio would move against governments in such times (since debts would go up, but economic growth would go down), thereby leading to higher interest rates and even larger deficits. Third, as deflation causes the real burden of debt to go up, it stands to benefit creditors – until defaults go up as a result, and bank failures follow. Fourth, real wages go up even as nominal wages stay constant – and from a tax collection standpoint, the government is not able to monetize that benefit. Inflation is the easy way, even if it just delays the day of reckoning. All worth keeping in mind, I think , any time you hear an economist or politician prattle on.

As a last anecdote, the author speculates that $9,000 per ounce for gold is closer to fair value given the global money supply.