In the comments section to this post on Zero Hedge, someone suggested that green energy is making serious progress and you should ignore it at your own risk. To which someone else responded...

"My car has solar panels installed on its roof. In sunshine, it almost creates sufficient energy to make it actually move. It's really good downhill, though."

I laughed out loud.

Wednesday, February 27, 2013

Tuesday, February 26, 2013

What's on my mind today

-I finished Opportunities in Emerging Markets by Gordian Gaeta (2013), which basically lays out the case for investing in those economies and ideas on how to do it. The first third largely reads like a textbook, and then loosens up a bit with chapters written by investment managers who focus on these locales. An interesting tidbit is that higher private equity flows into a developing market are often a precursor to future stock market growth for the country. Which, of course, speaks to the fact that a functioning and liquid stock market is also an important player in a country’s growth prospects. The advantages of these markets are faster growth, favorable demographics, healthier sovereign balance sheets, movement towards global integration, attractive market valuations, inefficient markets, and lower correlation to the rest of the world. As a generalization, investing in resource rich economies is a good idea. If I ever taught a class on the subject of frontier markets, I would probably include this book on the reading list.

-With the return of my leg injury, and no more running for a while, I am embracing the swimming pool again. Except, whereas last time I lost motivation, I am now paying someone to coach me through “training” for the swim portion of a triathlon. Hopefully I will do a better job of sticking with it and making it a permanent part of my future workout life.

-I fear trying to call a bottom in anything these days, but today’s piece out of the Casey group spoke of continued long term optimism for gold, but a greater sense that the bottom was not yet in. When the biggest gold bulls are acting cautious, is that what capitulation kind of looks like?

-With the return of my leg injury, and no more running for a while, I am embracing the swimming pool again. Except, whereas last time I lost motivation, I am now paying someone to coach me through “training” for the swim portion of a triathlon. Hopefully I will do a better job of sticking with it and making it a permanent part of my future workout life.

-I fear trying to call a bottom in anything these days, but today’s piece out of the Casey group spoke of continued long term optimism for gold, but a greater sense that the bottom was not yet in. When the biggest gold bulls are acting cautious, is that what capitulation kind of looks like?

Thursday, February 21, 2013

Jawboning

It's about 4 months old, but I stumbled onto the November 2012 client letter put out by Sitka Pacific Capital Management. Really interesting and does the best job I have seen lately of explaining why the Fed can never let up with money printing and debt monetization – at least, not until the currency or bond markets force it to. So, any recent conversation that it might happen, based on suggestions in the Fed minutes, is just more silliness along the lines of the “fiscal cliff”.

The key points:

-As we know, interest rates are very low. A partial implication is that the cost of debt is very cheap for Uncle Sam. But, conversely, in such a world, if rates are allowed to rise (and you are deluding yourself if you think rates would stay where they are without the Fed supporting the market), there is a spring-loaded effect on the budget. Each 100 bps move up equates to $160 billion more in interest expense (and that's only if you assume that debt levels stop increasing). Therefore, instead of the current $400 billion in annual interest expense, the number could easily shoot up to $1 trillion or more (representing some 40+% of collected taxes). That simply is not sustainable.

-The interest payments that the Fed receives on the debt that it buys are returned to the Treasury each year. Yet another reason that total interest expense in the federal budget is not higher. Thus, if the Fed stops buying and stops passing those coupon payments back, the budget deficit gets worse, even without a move in rates.

To be clear, these realities are not the hallmark of cyclical problems, but structural. The Fed is not going to end its game voluntarily.

The key points:

-As we know, interest rates are very low. A partial implication is that the cost of debt is very cheap for Uncle Sam. But, conversely, in such a world, if rates are allowed to rise (and you are deluding yourself if you think rates would stay where they are without the Fed supporting the market), there is a spring-loaded effect on the budget. Each 100 bps move up equates to $160 billion more in interest expense (and that's only if you assume that debt levels stop increasing). Therefore, instead of the current $400 billion in annual interest expense, the number could easily shoot up to $1 trillion or more (representing some 40+% of collected taxes). That simply is not sustainable.

-The interest payments that the Fed receives on the debt that it buys are returned to the Treasury each year. Yet another reason that total interest expense in the federal budget is not higher. Thus, if the Fed stops buying and stops passing those coupon payments back, the budget deficit gets worse, even without a move in rates.

To be clear, these realities are not the hallmark of cyclical problems, but structural. The Fed is not going to end its game voluntarily.

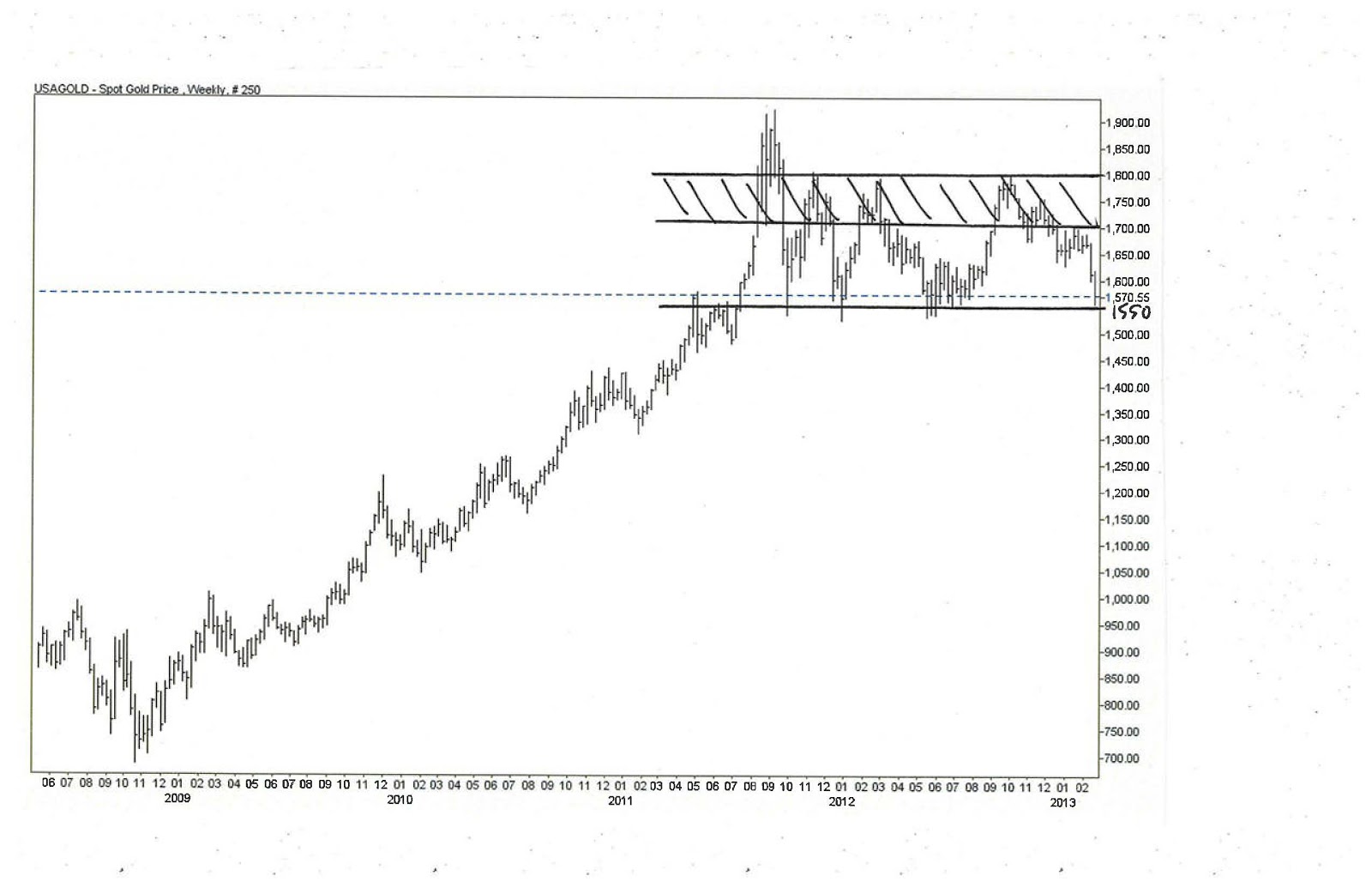

Yellow Dog Update

For my own edification, I decided to examine the gold chart to get a better handle on why I have been so wrong lately. I think I now understand why Faber saw $1,550 as the logical landing spot, if he was of the belief that the uptrend was not ready to resume yet.

Anyway, above is a weekly chart that dates back to mid-2008. What you’ll notice is a distinct uptrend that moved along in a consistent and measured way through the first half of 2011. Then, in the summer, there is a huge spike up that coincides with the sovereign debt downgrade. After that euphoria, gold falls into a range with about $1,550 on the bottom (the level where the spike started) and $1,800 on the top. Had it not been for the spike to $1,900+, the pattern since mid-2011 would look more like a consolidation pattern and likely would not engender the same degree of angst from gold bulls and bears alike. Maybe I’m stubborn, but I continue to believe that the fundamentals underlying a long gold position remain in place. Chart be damned.

But, turning to the technicals, I think Faber is right about where the support will kick in. It has done it at that level several times already over the past 2 years. On the upside, the band between $1,700 and $1,800 is where the struggle will occur. Using those levels, therefore, is how I might craft a trade.

Anyway, above is a weekly chart that dates back to mid-2008. What you’ll notice is a distinct uptrend that moved along in a consistent and measured way through the first half of 2011. Then, in the summer, there is a huge spike up that coincides with the sovereign debt downgrade. After that euphoria, gold falls into a range with about $1,550 on the bottom (the level where the spike started) and $1,800 on the top. Had it not been for the spike to $1,900+, the pattern since mid-2011 would look more like a consolidation pattern and likely would not engender the same degree of angst from gold bulls and bears alike. Maybe I’m stubborn, but I continue to believe that the fundamentals underlying a long gold position remain in place. Chart be damned.

But, turning to the technicals, I think Faber is right about where the support will kick in. It has done it at that level several times already over the past 2 years. On the upside, the band between $1,700 and $1,800 is where the struggle will occur. Using those levels, therefore, is how I might craft a trade.

Wednesday, February 20, 2013

Blood in the Streets

I think we may have reached a bottom. And, by that, I mean emotional. Not only am I getting buzz-sawed in the markets, but it turns out that I have re-injured my leg. And this too shall pass.

Faber's Prediction

I went back to check what Faber's most recent prediction was for gold. As you'll recall, I mentioned that on numerous occasions over the past 6-8 months he had pegged about $1,550 as the bottom for the most recent correction. In his February market commentary, with the price at about $1,660 or so, he anticipated another $50 to $100 down. With today, it looks like he got his wish.

Currency Wars

I offer four charts for your consideration.

1) British Pound

2) Euro

3) Yen

4) Gold (using GLD as proxy)

Each tells an interesting story. In Europe, where the Eurozone is in the midst of a depression and the threat of money-printing has not yet been implemented, the currency is getting stronger against the dollar. Conversely, the pound and the yen speak to a strengthening dollar (as those countries have gotten more serious about debasement), which is kind of the opposite of what the U.S. wants. And, gold, well, people just don't like it right now and the weak hands (and probably some strong ones as well) are being flushed out. Somehow people think that the liquidity explosion the world over is going to slow down here. I think that is a bad assumption.

1) British Pound

2) Euro

3) Yen

4) Gold (using GLD as proxy)

Each tells an interesting story. In Europe, where the Eurozone is in the midst of a depression and the threat of money-printing has not yet been implemented, the currency is getting stronger against the dollar. Conversely, the pound and the yen speak to a strengthening dollar (as those countries have gotten more serious about debasement), which is kind of the opposite of what the U.S. wants. And, gold, well, people just don't like it right now and the weak hands (and probably some strong ones as well) are being flushed out. Somehow people think that the liquidity explosion the world over is going to slow down here. I think that is a bad assumption.

Quote of the Day

Courtesy of Robert Kaplan at Stratfor:

"...the most profound lesson of Thucydides and Hobbes is to concentrate on what goes unstated in crises, on what can only be deduced. For the genius of analysis lies in quiet deductions, not in the mere parroting of public statements. What starts conflicts is public, and therefore much less interesting - and less crucial - than the causes of conflicts, which are not often public."

Strikes me as the type of comment that applies equally to global conflict as to investment considerations that follow from policy solutions.

"...the most profound lesson of Thucydides and Hobbes is to concentrate on what goes unstated in crises, on what can only be deduced. For the genius of analysis lies in quiet deductions, not in the mere parroting of public statements. What starts conflicts is public, and therefore much less interesting - and less crucial - than the causes of conflicts, which are not often public."

Strikes me as the type of comment that applies equally to global conflict as to investment considerations that follow from policy solutions.

Sunday, February 17, 2013

Catastrophic Care

I never thought I would enjoy a book about the U.S. health care system so much, but David Goldhill writes really well. In Catastrophic Care (2013), he explains why the system is so screwed up and then offers some ideas on how to fix it. He isn’t an economist or doctor, in fact he works in the cable business, but in 2007 his father died as a result of mistakes made while being treated in a NY hospital. This book is his attempt to do something about it. As with the John Goodman book that I wrote about previously, I’m not operating with a knowledge base that allows me to challenge the nuances that Goldhill goes through, but a lot of what he says sounds pretty familiar and intuitively makes a lot of sense. So, without further ado, what follows is a random assortment of Goldhill’s most salient observations:

-The basic problem is not a lack of access to insurance, but insurance itself, which drives overtreatment, cost inflation and mistakes. Health care is not the same thing as health insurance.

-Most of the cost to individuals is disguised. The contribution you make goes beyond premiums. For starters, often an employer is responsible for paying much of an employee’s coverage, meaning the employer will pay a lower salary. Furthermore, everyone with a paycheck pays the Medicare Part A tax; in addition, 20% of the federal budget (and 10% for the states) is health care related, so a large chunk of income taxes goes towards those costs.

-The health care system is one where patients largely expect someone else to pay, so the typical dynamics operating in the market and which compel service providers to offer better quality at lower prices just don’t exist. And as insurance companies are on the hook, they simply turn around and charge higher premiums to compensate for the overtesting and cost inflation that exists.

-With someone else paying, consumers are less apt to question whether a test is really needed and to shop around. Moreover, doctors (and consequently insurers who will charge higher premiums) are only too happy for yet another condition to emerge (think erectile dysfunction) where a new treatment is discovered. Goldhill calls it the growth of chronic conditions and the reclassification of medical definitions. Under these circumstances, eventually everyone gets hit with the diagnosis of some chronic condition that requires treatment – even, if historically, it was something that people just lived with.

-With Medicare, even though seniors only pay a small percentage of costs, the explosion in medical services overall has led to a greater burden as a percentage of total income.

-One criticism of private insurance (versus Medicare or Medicaid) is that administrative costs are much higher. But, by virtue of having lower costs, these public insurers have far less oversight and the degree of fraud is meaningfully greater.

-Medicare is funded in three ways: the payroll tax, monthly premiums paid by seniors, and general government revenues. It is often mentioned that Part A pays for itself through the payroll tax (and in fact generates a surplus). But, since 2007, each year that surplus has been lent out to the rest of the government to pay for our huge deficits – the trust fund is now filled with IOUs. Now, question whether you really think that means public health care has sound financing and is self-sustaining. In 2009, the Medicare trustee estimated the future shortfall to be $36 trillion, and then subsequently acknowledged that it is likely understating what the true cost will be. The mistake, as Goldhill notes, is that the government continually assumes that there is some fixed amount of health care needed, but “need” just keeps growing. And a third party payer system is largely at fault.

-The system has this funky way of paying specialists more than general practitioners, which means the more personalized area of medicine, where there possibly exists an intermediary best placed to correlate all the various symptoms, is paid less and thus finds fewer new doctors entering its ranks.

-The uninsured are usually those most likely to shop around and demand lower pricing for services rendered. Under Obamacare, and the mandate that everyone has to have insurance, these discounted people are suddenly going to be full-priced customers, creating even more health care inflation.

-Obamacare mistakenly assumes that an increase in preventive care will lower overall costs. Except what probably happens is that healthy people, who aren’t at risk in the first place, will end up getting more tests, driving up the expense.

-When pundits talk about it, don’t be misled. Costs in other countries only seem under control when compared with the United States. Globally, no system has managed to keep expenses in check, other than perhaps Singapore which has far less in the way of subsidies.

-Obamacare could very well lead to fewer people with insurance. First off, the penalties on individuals for not buying insurance are de minimis enough to go without until insurance is needed; especially since once you need it, a preexisting condition can no longer be the basis for a denial. Similarly, the penalty on employers for not providing insurance is small enough that the arithmetic makes it cost-efficient to pay a slightly higher salary and to send employees to the health care exchanges. From the standpoint of the private insurers, since they are now blindly bidding on these exchanges for new beneficiaries, without being able to assess risk profiles, they certainly have no incentive to be competitive on what sorts of premiums they offer. How does that bring costs down?

Now on to his suggestions for change. Trying to insure everything makes it much more difficult and expensive to protect against true catastrophes. Goldhill proposes a system where individuals have to pay more out of pocket for the anticipated expenses. If everyone had health savings accounts to pay for preventive care, which receive the same tax advantaged status of employer insurance, people would be cognizant of cost and quality. In addition, insurance’s role would be limited to the truly unforeseen, meaning a higher deductible and lower premiums. In this scenario, we remove the passive third party payer and market forces are allowed to work. There’s more to it, but I guess you’ll have to read the book to find out.

Anyway, a really important work that everyone should read.

-The basic problem is not a lack of access to insurance, but insurance itself, which drives overtreatment, cost inflation and mistakes. Health care is not the same thing as health insurance.

-Most of the cost to individuals is disguised. The contribution you make goes beyond premiums. For starters, often an employer is responsible for paying much of an employee’s coverage, meaning the employer will pay a lower salary. Furthermore, everyone with a paycheck pays the Medicare Part A tax; in addition, 20% of the federal budget (and 10% for the states) is health care related, so a large chunk of income taxes goes towards those costs.

-The health care system is one where patients largely expect someone else to pay, so the typical dynamics operating in the market and which compel service providers to offer better quality at lower prices just don’t exist. And as insurance companies are on the hook, they simply turn around and charge higher premiums to compensate for the overtesting and cost inflation that exists.

-With someone else paying, consumers are less apt to question whether a test is really needed and to shop around. Moreover, doctors (and consequently insurers who will charge higher premiums) are only too happy for yet another condition to emerge (think erectile dysfunction) where a new treatment is discovered. Goldhill calls it the growth of chronic conditions and the reclassification of medical definitions. Under these circumstances, eventually everyone gets hit with the diagnosis of some chronic condition that requires treatment – even, if historically, it was something that people just lived with.

-With Medicare, even though seniors only pay a small percentage of costs, the explosion in medical services overall has led to a greater burden as a percentage of total income.

-One criticism of private insurance (versus Medicare or Medicaid) is that administrative costs are much higher. But, by virtue of having lower costs, these public insurers have far less oversight and the degree of fraud is meaningfully greater.

-Medicare is funded in three ways: the payroll tax, monthly premiums paid by seniors, and general government revenues. It is often mentioned that Part A pays for itself through the payroll tax (and in fact generates a surplus). But, since 2007, each year that surplus has been lent out to the rest of the government to pay for our huge deficits – the trust fund is now filled with IOUs. Now, question whether you really think that means public health care has sound financing and is self-sustaining. In 2009, the Medicare trustee estimated the future shortfall to be $36 trillion, and then subsequently acknowledged that it is likely understating what the true cost will be. The mistake, as Goldhill notes, is that the government continually assumes that there is some fixed amount of health care needed, but “need” just keeps growing. And a third party payer system is largely at fault.

-The system has this funky way of paying specialists more than general practitioners, which means the more personalized area of medicine, where there possibly exists an intermediary best placed to correlate all the various symptoms, is paid less and thus finds fewer new doctors entering its ranks.

-The uninsured are usually those most likely to shop around and demand lower pricing for services rendered. Under Obamacare, and the mandate that everyone has to have insurance, these discounted people are suddenly going to be full-priced customers, creating even more health care inflation.

-Obamacare mistakenly assumes that an increase in preventive care will lower overall costs. Except what probably happens is that healthy people, who aren’t at risk in the first place, will end up getting more tests, driving up the expense.

-When pundits talk about it, don’t be misled. Costs in other countries only seem under control when compared with the United States. Globally, no system has managed to keep expenses in check, other than perhaps Singapore which has far less in the way of subsidies.

-Obamacare could very well lead to fewer people with insurance. First off, the penalties on individuals for not buying insurance are de minimis enough to go without until insurance is needed; especially since once you need it, a preexisting condition can no longer be the basis for a denial. Similarly, the penalty on employers for not providing insurance is small enough that the arithmetic makes it cost-efficient to pay a slightly higher salary and to send employees to the health care exchanges. From the standpoint of the private insurers, since they are now blindly bidding on these exchanges for new beneficiaries, without being able to assess risk profiles, they certainly have no incentive to be competitive on what sorts of premiums they offer. How does that bring costs down?

Now on to his suggestions for change. Trying to insure everything makes it much more difficult and expensive to protect against true catastrophes. Goldhill proposes a system where individuals have to pay more out of pocket for the anticipated expenses. If everyone had health savings accounts to pay for preventive care, which receive the same tax advantaged status of employer insurance, people would be cognizant of cost and quality. In addition, insurance’s role would be limited to the truly unforeseen, meaning a higher deductible and lower premiums. In this scenario, we remove the passive third party payer and market forces are allowed to work. There’s more to it, but I guess you’ll have to read the book to find out.

Anyway, a really important work that everyone should read.

Friday, February 15, 2013

Fortunately, a long weekend to recover...

Bill Fleckenstein wrote a thoughtful piece today on the heels of gold getting smacked around, as has been its wont.

(To be noted up front: I have been completely and utterly wrong lately, lest anyone think I am trying to avoid the obvious. My predictions of $2,000 gold, the call positions I put on, all of it…WRONG, WRONG, WRONG!!)

He notes that we see the ingredients that led to the previous two bubbles front and center again, so invariably we will end up in the same place. And that’s kind of the point here. It’s what I was trying to get at with my post about Krugman yesterday. The economists and central planners who run this spot always default to the same solutions and remedies. Even when a sample size in the trillions of dollars doesn’t get the desired result. Eventually it catches up to us and inflation gets out of control and markets go haywire. All of which plays into the hands of gold.

Or so I’m banking on.

One last thing – Marc Faber is definitely a smart guy. The next time he writes that gold will correct down to $1,550 or so (and he did it for months on end), I’ll defer to his wisdom and experience on the subject.

(To be noted up front: I have been completely and utterly wrong lately, lest anyone think I am trying to avoid the obvious. My predictions of $2,000 gold, the call positions I put on, all of it…WRONG, WRONG, WRONG!!)

He notes that we see the ingredients that led to the previous two bubbles front and center again, so invariably we will end up in the same place. And that’s kind of the point here. It’s what I was trying to get at with my post about Krugman yesterday. The economists and central planners who run this spot always default to the same solutions and remedies. Even when a sample size in the trillions of dollars doesn’t get the desired result. Eventually it catches up to us and inflation gets out of control and markets go haywire. All of which plays into the hands of gold.

Or so I’m banking on.

One last thing – Marc Faber is definitely a smart guy. The next time he writes that gold will correct down to $1,550 or so (and he did it for months on end), I’ll defer to his wisdom and experience on the subject.

Thursday, February 14, 2013

Both Sides of Your Mouth

I found the point of this recent Paul Krugman blog post to be incredibly rich.

In it, he calls out all the folks who didn’t see the housing bubble for what it was. The funny part is that Krugman is trying very hard to lord over people that they didn’t see something that he himself asked for in a 2002 piece (even though subsequently he has tried to hem and haw on what he meant).

It gets even better, though, because in examining a 2005 piece, where he very much calls housing a bubble (kudos to him), he worries that there won’t be yet another bubble to replace housing, which replaced stocks. So, wait a minute. A bubble is a bad thing. You take people to task for missing it. Yet, your strategy for more than a decade has been to create more of them in succession.

In it, he calls out all the folks who didn’t see the housing bubble for what it was. The funny part is that Krugman is trying very hard to lord over people that they didn’t see something that he himself asked for in a 2002 piece (even though subsequently he has tried to hem and haw on what he meant).

It gets even better, though, because in examining a 2005 piece, where he very much calls housing a bubble (kudos to him), he worries that there won’t be yet another bubble to replace housing, which replaced stocks. So, wait a minute. A bubble is a bad thing. You take people to task for missing it. Yet, your strategy for more than a decade has been to create more of them in succession.

Wednesday, February 13, 2013

Japan Update

I listened in on a webinar today about the future of the Yen and JGB markets. Generally, the speakers were in agreement that the Yen would continue to weaken (and eventually so will JGBs), which syncs with my view. But the knock-on consequence that was mentioned, and which was a new twist for me, was that all the Yen liquidity to come would need a deep market to go into, and one possible venue would be U.S. Treasuries. The implication is that rates in the U.S. are likely to stay low for a while (which reminds me of one argument from the Richard Duncan book).

The other point is that a currency crisis sets off a debt crisis (and vice versa). If interest rates start to kick up and the Central Bank tries to defend the market by printing endless currency units to buy bonds, the resulting devaluation of the currency increases inflation expectations and thereby causes rates up anyway.

As far as timing, the Yen will crack first, so get long some long-dated Yen puts as a first step. The other really compelling idea is to figure out a way to get short Yen in gold terms (which is not easy to execute at this point).

The other point is that a currency crisis sets off a debt crisis (and vice versa). If interest rates start to kick up and the Central Bank tries to defend the market by printing endless currency units to buy bonds, the resulting devaluation of the currency increases inflation expectations and thereby causes rates up anyway.

As far as timing, the Yen will crack first, so get long some long-dated Yen puts as a first step. The other really compelling idea is to figure out a way to get short Yen in gold terms (which is not easy to execute at this point).

Talking Health Care

I am in the middle of a really interesting and well-done book about the U.S. health care system called Catastrophic Care by David Goldhill (2013). I plan to do a full write-up when done, but still thought it worthwhile to mention a very important point that Goldhill makes. In the context of insurance, it is really a very recent phenomenon (basically the past 45 years). And in that period is when we have seen the greatest surge in health care inflation. The issue, as Goldhill sees it, is that the insurance companies are in the business of making money through premiums. And they can only really raise premiums if more money is spent on health care in general. So, while they may talk a good game about healthy living and exercise, they are a much happier group if people need doctors and more procedures are approved and need to be administered. For those who then argue that that would imply that the government should become the single payer, tell me in what universe the folks who run Medicare or Medicaid will ever start worrying about efficiencies when they have an unlimited budget and will have to face a little special interest group comprised of all senior citizens if they ever do try to cut back. The end game is higher health care costs. Obamacare largely just added to the base of people that insurance companies will be able to collect premiums from.

More to come.

More to come.

Tuesday, February 12, 2013

Price Action in Gold

Let me start out by saying that I think the bull market in gold has not ended. And with the distortions that continue to build up across the economy, it stands to reason that the price will eventually go much higher.

Nevertheless, anyone paying attention knows that the price has essentially stagnated for the past 17 or so months following the high of $1,921 hit in the fall of 2011. In more recent times, as people seem to be getting comfortable with the notion that the economy is healing and better times lie ahead (as evidenced by slightly increasing bond yields and happy days in the stock market), gold is still moving sideways. So, if I were looking for a sign that gold is at a tenuous point, it is that I would have expected the yellow dog to participate in the party. And that it hasn’t is a slight rebuke of my thesis.

But that’s what makes markets. Gold remains the contrarian play (until otherwise noted).

In any event, I looked at the chart today and think the price has bottomed for this period of the cycle. Might I be wrong? Sure. But, I don’t think that it would be a very big deal if I am. Chart below for reference (using GLD as proxy) and it bounced on an important trend line that dates back for years. The one caveat is that a trend line can better be thought of as a region of support, meaning the price might flirt a little bit below in days ahead. That would be alright.

Nevertheless, anyone paying attention knows that the price has essentially stagnated for the past 17 or so months following the high of $1,921 hit in the fall of 2011. In more recent times, as people seem to be getting comfortable with the notion that the economy is healing and better times lie ahead (as evidenced by slightly increasing bond yields and happy days in the stock market), gold is still moving sideways. So, if I were looking for a sign that gold is at a tenuous point, it is that I would have expected the yellow dog to participate in the party. And that it hasn’t is a slight rebuke of my thesis.

But that’s what makes markets. Gold remains the contrarian play (until otherwise noted).

In any event, I looked at the chart today and think the price has bottomed for this period of the cycle. Might I be wrong? Sure. But, I don’t think that it would be a very big deal if I am. Chart below for reference (using GLD as proxy) and it bounced on an important trend line that dates back for years. The one caveat is that a trend line can better be thought of as a region of support, meaning the price might flirt a little bit below in days ahead. That would be alright.

Human Psychology

In less than 3 months, the Japanese Yen has moved from 79 to 94. A huge move in terms of currencies. And for those who read this site regularly, I had been arguing for a while that such a move was coming. Add to that, I commented at the outset of 2013 that short Yen would be a great levered trade. So, why then haven’t I done much to capture it? I had a small put position on FXY that made a bit of money, but closed it out in January very early. And since then I have just watched as the currency seems to implode on itself.

When Shinzo Abe announced in November that he was running his campaign on the premise that he could raise inflation in Japan from 1% to 2 or 3%, the next era in a world of money-printing was set to be unleashed. As compared to the U.S., Japan’s debt-to-GDP levels and demographics are further along in the process of becoming unhinged. So announcements of the sort by Abe and subsequent implementation push that country even further towards a crisis of some sort. Starting with the currency. And at the point where control over exchange rates is lost, it becomes very hard for anyone to get it back.

And I knew this and thought I would strike when the moment finally arrived. But, I hesitated. Apparently I am subject to the same flaws of human nature as everyone else. I’d rather be wrong or miss out on an opportunity with the majority, then step up and fail greatly (or succeed greatly, as the case may be with the Yen).

The other possibility is that I am like most folks who look at gold as it continues to rise and still won’t buy just because it seems like so much has happened already. But, when a trend begins, it often continues for a long time. We are at the crescendo moment for the big economies that have been relying on a printing press for several decades. I even said last year that it would start in Japan before it hit my shores. So, maybe I need to wake up to my own advice.

I feel like I let myself down here. I will try not to let it happen again.

When Shinzo Abe announced in November that he was running his campaign on the premise that he could raise inflation in Japan from 1% to 2 or 3%, the next era in a world of money-printing was set to be unleashed. As compared to the U.S., Japan’s debt-to-GDP levels and demographics are further along in the process of becoming unhinged. So announcements of the sort by Abe and subsequent implementation push that country even further towards a crisis of some sort. Starting with the currency. And at the point where control over exchange rates is lost, it becomes very hard for anyone to get it back.

And I knew this and thought I would strike when the moment finally arrived. But, I hesitated. Apparently I am subject to the same flaws of human nature as everyone else. I’d rather be wrong or miss out on an opportunity with the majority, then step up and fail greatly (or succeed greatly, as the case may be with the Yen).

The other possibility is that I am like most folks who look at gold as it continues to rise and still won’t buy just because it seems like so much has happened already. But, when a trend begins, it often continues for a long time. We are at the crescendo moment for the big economies that have been relying on a printing press for several decades. I even said last year that it would start in Japan before it hit my shores. So, maybe I need to wake up to my own advice.

I feel like I let myself down here. I will try not to let it happen again.

Monday, February 11, 2013

Quote of the Day

It was a tie today...

"A ship in the harbor is safe, but that is not what ships are built for."

-William G.T. Shedd

"None of us will ever accomplish anything excellent or commanding except when he listens to this whisper which is heard by him alone."

-Ralph Waldo Emerson

"The man who thinks he can and the man who thinks he can't are both right. Which one are you?"

-Henry Ford

"A ship in the harbor is safe, but that is not what ships are built for."

-William G.T. Shedd

"None of us will ever accomplish anything excellent or commanding except when he listens to this whisper which is heard by him alone."

-Ralph Waldo Emerson

"The man who thinks he can and the man who thinks he can't are both right. Which one are you?"

-Henry Ford

Wednesday, February 6, 2013

Call Me Ted

On a recent long flight, I finished the Ted Turner autobiography (2008). Generally, I find it useful to hear how very successful people think about the world. In Turner's case, the main takeaway is that he is perpetually looking for opportunities, and in the face of many setbacks and daunting odds always goes full throttle after what he believes in. Good advice, I think.

Subscribe to:

Comments (Atom)

-

Are when the contrarian should think about buying. And so I tried. Some AUY LEAPS (filled) and a small mining services company that I like...

-

I came across this really interesting chart regarding 2013 and 2014 EPS forecasts by region and globally. Note the very pronounced move fr...

I came across this really interesting chart regarding 2013 and 2014 EPS forecasts by region and globally. Note the very pronounced move fr... -

Lately, in spite of various frustrations, I have been trying to think through where the opportunities will be in real estate. We’ve discuss...